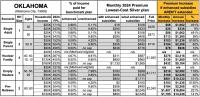

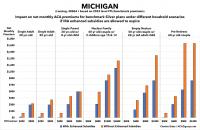

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

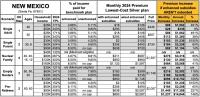

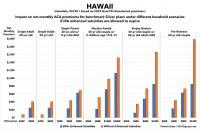

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

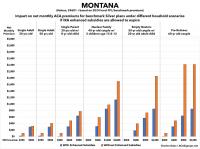

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

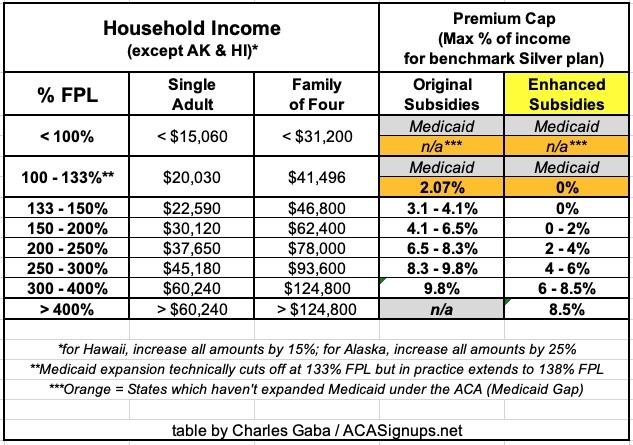

This is, of course, extremely important since household income is one of the most critical factors in calculating how much financial assistance enrollees receive (or if they're eligible for Advance Premium Tax Credits (ATPC) at all).

If you've ever wondered why healthcare wonks (myself included) almost never even bring up the ACA's Catastrophic Level plans and why the only time I ever discuss Platinum Plans is in the context of high-CSR enrollees being eligible for "Secret Platinum" plans (labeled as Silver), this table should explain why.