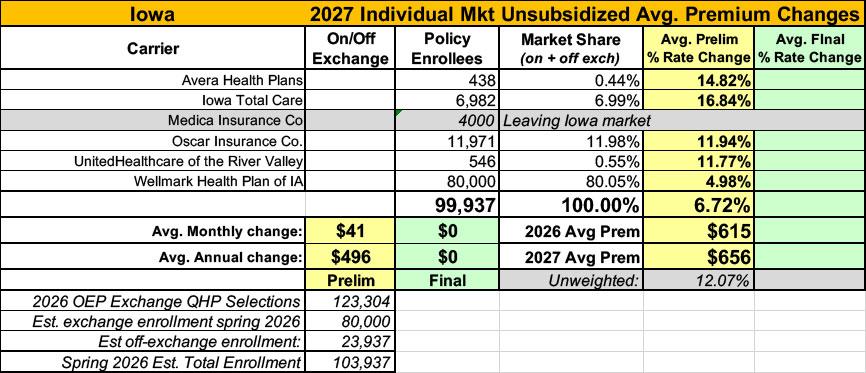

2027 Rate Changes - Iowa +6.7% for unsubsidized indy market enrollees; Medica is out

Mon, 07/13/2026 - 4:35pm

ACA Individual Market — 2027 filings subject to rate hearings:

- Avera Health Plans — 14.82% average increase on 438 lives; range of 12.30% to 21.70%

- Iowa Total Care, Inc. — 16.84% average increase on 6,982 lives; range of 9.39% to 21.75%

- Oscar Insurance Company — 11.94% average increase on 11,971 lives; range of 4.63% to 28.17%

- UnitedHealthcare Plan of the River Valley — 11.77% average increase on 546 lives; range of 9.66% to 12.53%

- Wellmark Health Plan of Iowa — 4.98% average increase on approximately 80,000 lives; range of -2.27% to 10.73%; on-Exchange

As for Medica, which has around 4,000 Iowa enrollees this year...

Medica will no longer offer individual marketplace plans in Iowa, Kansas and Oklahoma, effective January 1, 2027.

The decision affects about 4,000 members in Iowa, 600 members in the Kansas City area in Kansas, and 8,400 members in Oklahoma, the company confirmed to Becker’s. The insurer will continue to offer marketplace coverage in Minnesota, Missouri, Nebraska, North Dakota and Wisconsin.

“Members currently enrolled in Medica individual products in these states will continue to receive benefits until their renewal date,” a Medica spokesperson said. “Medica’s strategic focus is to ensure we remain competitive in markets where we can deliver value by simplifying offerings, reducing overlap, and prioritizing high-value provider partnerships.”

This puts Iowa's total ACA-compliant individual market at around 104,000 people total as of spring 2026, with preliminary weighted average 2027 rate increases of around 6.7%...the second-lowest statewide average I've seen so far, after Vermont's 6.5% average:

Avera Health Plans:

1. SCOPE AND RANGE OF RATE INCREASE

Avera Health Plans, Inc. (Avera) is requesting a rate increase for the Avera MyPlan individual products for Iowa with an effective date of January 1, 2027. The requested overall rate increase impacts approximately 438 members. The rate increase being requested for the Avera MyPlan products is 14.8% averaged across all members. Rate changes vary by plan due to changes in cost sharing parameters (e.g., deductible, coinsurance, copays) relative to 2026 cost sharing parameters, ranging from 12.3% to 21.7% by plan.

2. FINANCIAL EXPERIENCE

There is no historical financial experience to report as Avera entered the Iowa individual market on January 1, 2026. The financial experience for Avera’s South Dakota individual ACA-compliant experience, which supports manual rate projections in Iowa, was unfavorable in 2025 relative to the 2024 experience used to develop 2026 rates.

3. CHANGES IN MEDICAL SERVICE COSTS AND TREND ASSUMPTIONS

To capture the increasing cost and utilization of medical services, projections from manual rate experience assume 6.7% annual trend. This assumption is based on analysis of regional and national trends and actuarial judgment.

4. CHANGES IN BENEFITS

Avera will make cost sharing modifications by plan to comply with the final 2027 Actuarial Value Calculator and based on 2027 strategic considerations. To the extent the plan changes lead to a higher or lower level of benefit richness, the premium rates would increase or decrease, respectively.

5. ADMINISTRATIVE COSTS AND ANTICIPATED PROFITS

Avera is targeting a loss ratio of 86.5% for its individual block of business in January 2027. This loss ratio allows 13.5% for total health plan administrative costs, taxes, fees, and anticipated profits.

6. EXPIRATION OF EXPANDED ADVANCE PREMIUM TAX CREDIT SUBSIDIES

Avera expects the expiration of expanded Advance Premium Tax Credit subsidies will result in higher market morbidity due to the anticipated mix of enrollees remaining in the market.

IOWA TOTAL CARE:

Iowa Total Care is filing rates for the individual block of business, effective January 1, 2027. This document is submitted in conjunction with the Part I Unified Rate Review Template and the Part III Actuarial Memorandum.

This information is intended for use by the Iowa Insurance Division, the Center for Consumer Information and Insurance Oversight (CCIIO), and health insurance consumers in Iowa to assist in the review of Iowa Total Care’s individual rate filing.

The results are actuarial projections. Actual experience will differ for a number of reasons, including population changes, claims experience, and random deviations from assumptions.

In 2025, earned premium was $517.11 per member per month (PMPM). Incurred claims in 2025 were $363.50, or 70.29% of premium. Netting risk adjustment from the claims results in an estimated loss ratio (incurred claims net of estimated risk adjustment transfers, divided by earned premiums) of 80.67%. We expect unit costs to increase for 2027. Further, we have updated underlying experience for the single risk pool, expected administrative expense, and assumptions for federal risk adjustment. These factors, as well as changes to the assumed morbidity of the single risk pool and medical trend, result in a premium rate increase.

Medical trend, or the increase in health care costs over time, is composed of two components: the increase in the unit cost of services and the increase in the utilization of those services. Unit cost increases occur as care providers and their suppliers raise their prices. Utilization increases can occur as people seek more services than before. Additionally, simple services can be replaced with more complex services over time, which is known as service intensity trend. An example of service intensity trend would be the replacement of an X-ray with an MRI scan. Replacing the service with a more intense service causes the total cost of medical services to increase.

The proposed rate change of 16.8% applies to approximately 6,982 individuals. Iowa Total Care’s projected administrative expenses for 2027 are $100.80 PMPM. Administrative expense does not include $19.87 for taxes and fees. The historical administrative expenses for 2026 were $81.57 PMPM, which excludes taxes and fees. The projected loss ratio is 81.0% which satisfies the federal minimum loss ratio requirement of 80.0%.

OSCAR INSURANCE CO:

1. Scope and Range of Rate Increase

The purpose of this document is to present rate change justification for Oscar Insurance Company, Inc (Oscar’s) Individual Affordable Care Act (ACA) products, with an effective date of January 1, 2027, and to comply with the requirements of Section 2794 of the Public Health Service Act as added by Section 1003 of the Patient Protection and Affordable Care Act (ACA).

Using in-force business as of March 2026, the proposed average rate increase for renewing plans is 11.9%. Rate increases vary by plan and range from 4.6% to 28.2% due to a combination of factors including shifts in benefit leveraging and cost-sharing modifications and network changes. This rate increase is absent of rate changes due to attained age. There are 11,971 current members impacted by this rate increase.

2. Reason for Rate Increase(s)

The significant factors driving the proposed rate change include the following:

Medical and Prescription Drug Infl ation and Utilization Trends

The projected premium rates reflect the most recent emerging experience which was trended for anticipated changes due to medical and prescription drug inflation and utilization.Administrative Expenses, Taxes and Fees, and Risk Margin

Changes to the overall premium level are needed because of required changes in federal and state taxes and fees. In addition, there are anticipated changes in both administrative expenses and targeted risk margin.Prospective Benefit Changes

Plan benefits have been revised as a result of changes in the Center for Medicare and Medicaid Services (CMS) Actuarial Value Calculator and state requirements, as well as for strategic product considerations.Anticipated Changes in the Average Morbidity of the Covered Population

Changes to the overall premium level are needed because of anticipated changes in the underlying morbidity of the projected marketplace.Anticipated Changes in the Network Configuration

Changes to the overall premium level are needed because of anticipated changes in the underlying network configuration and associated unit costs.

UNITEDHEALTHCARE OF THE RIVER VALLEY:

Scope and Range of the Rate Increase

UHCPRV is filing 2027 rates for individual products. The proposed rate change is 11.77% and will affect 546 individuals. The rate changes vary between 9.66% and 12.53%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

Financial Experience of the Product

The premium collected in plan year 2025 was $3,966,129. Incurred claims during this period were $3,070,089 and UHCPRV expects payments of $42,830 for risk adjustment. The loss ratio, or portion of premium required to pay medical claims, for plan year 2025 is 78.49%.

Changes in Medical Service Costs

There are many different healthcare cost trends that contribute to increases in the overall U.S. healthcare spending each year. These trend factors affect health insurance premiums, which can mean a premium rate increase to cover costs. Some of the key healthcare cost trends that have affected this year’s rate actions include:

- Increasing cost of medical services: Annual increases in reimbursement rates to healthcare providers, such as hospitals, doctors, and pharmaceutical companies.

- Increased utilization: The number of office visits and other services continues to grow. In addition, total healthcare spending will vary by the intensity of care and use of different types of health services. The price of care can be affected using expensive procedures such as surgery versus simply monitoring or providing medications.

- Higher costs from deductible leveraging: Healthcare costs continue to rise every year. If deductibles and copayments remain the same, a higher percentage of healthcare costs need to be covered by health insurance premiums each year.

- Impact of new technology: Improvements to medical technology and clinical practice often result in the use of more expensive services, leading to increased healthcare spending and utilization.

- Legislative & regulatory changes: Premiums reflect an increase in projected average cost per member driven by adverse morbidity impacts associated with the expiration of enhanced APTCs and changes in federal premium subsidy eligibility.

WELLMARK HEALTH PLAN OF IA:

Scope and Range of Rate Increase

Wellmark Health Plan of Iowa, Inc. (Wellmark) has requested an average rate increase of 5.0% for ACA-compliant policies effective January 1, 2027. Rate increases vary by plan, ranging from -2.3% to 10.7%, and do not include rate changes due to age of the members on the policy. As of March 31st, 2026, there are approximately 80,000 individual members in the pool. Most of the members in the pool are eligible for a premium subsidy and may not experience a post-subsidy rate change within the range above.

- Financial Experience of the Product

Wellmark anticipates 2026 experience will be worse than the target loss ratio. Applying the requested rate increases, Wellmark projects a loss ratio of 89% for this block of business in 2027. It should be noted that the projected Medical Loss Ratio (MLR) meets the minimum requirement of 80% defined in the ACA.

- Changes in Medical Service Costs

Annual trend of 4.5% was used to project claims from the experience period into the rating period and drives rates up for 2027. This trend assumption includes changes in service costs and utilization.

- Changes in Benefits

Plan design changes were made to Wellmark’s 2027 product offerings. These changes drive rates down for 2027. Rate changes provided above incorporate the impact of plan design changes.

- Administrative Costs and Anticipated Profits

The main drivers of administrative expenses are employee salaries and benefits, broker and agent commissions, and various governmental taxes and fees. Wellmark strives to maintain a low administrative expense as a percent of premium, as well as the underlying cost of care, in order to provide the best value to our customers. With a decrease to the Exchange User Fee, smaller government fees in 2027 are driving rates down.

- American Rescue Plan Enhanced Subsidy Expiration

The enhanced subsidies afforded in the American Rescue Plan expired in 2026. Wellmark anticipates this change will result in worse market risk, driving rates up.

Advertisement