How much more are ~55,000 WEST VIRGINIA ACA enrollees *really* paying this year due to Trump/GOP policies?

Thu, 07/02/2026 - 12:48pm

IMPORTANT: See the original post in this series for an explanation of the methodology.

Regular readers know that I've been obsessing over the massive increases in both gross as well as net premiums for ACA health insurance policy enrollees being caused by the combination of Congressional Republicans allowing the enhanced federal tax credits to expire as well as other Trump Regime policy changes for well over a year and a half now.

I've written countless analyses of how much both gross and net premiums skyrocketed from 2025 to 2026 across different states, different income levels and various other demographics...and recently it was confirmed that over 2.6 million ACA exchange enrollees had already been priced out of the market as of February, with the number almost certain to climb further throughout the rest of 2026.

As I've repeatedly warned, however, the increases in premium costs (whether gross or net) are only half the story. The other big shoe which is dropping this year is increased out of pocket costs as millions of the ~19.2 million or so remaining enrollees as of February have been forced to downgrade their coverage to avoid (or at least minimize) those massive premium spikes.

In most cases this means moving to plans with higher deductibles, higher co-pays & higher coinsurance costs. In many cases this has also included moving to plana with worse networks, referral requirements to see specialists and so on.

With that in mind, that's exactly what I've decided to set out to do: Calculate the average year over year increase not just in net premiums (that is, how much more ACA enrollees are having to pay each month) but also the year over year change in average out of pocket costs.

Let's look at WEST VIRGINIA.

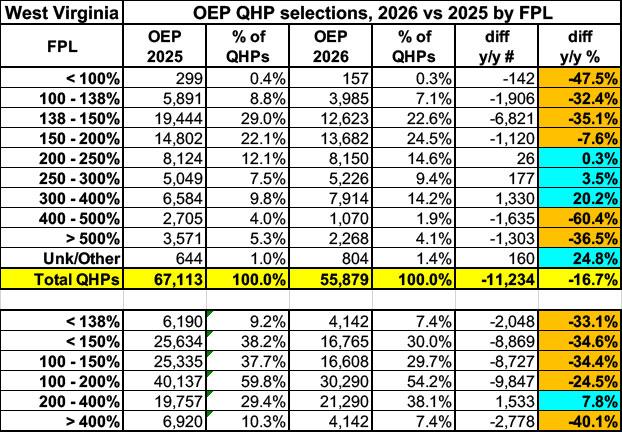

Here's a look at ACA exchange plan selections during Open Enrollment by household income level this year vs. last.

Like most states, West Virginia has seen enrollment plummet across most income brackets, especially among those earning more than 400% of the Federal Poverty Level. This is completely understandable given that WV has by far the most expensive unsubsidized ACA premiums in the country at over $1,300 per person on average.

Overall, plan selections during Open Enrollment dropped by 16.7%, or over 11,000 people versus OEP 2025...and since then, effectuated enrollment has almost certainly dropped further yet.

Onto the main analysis:

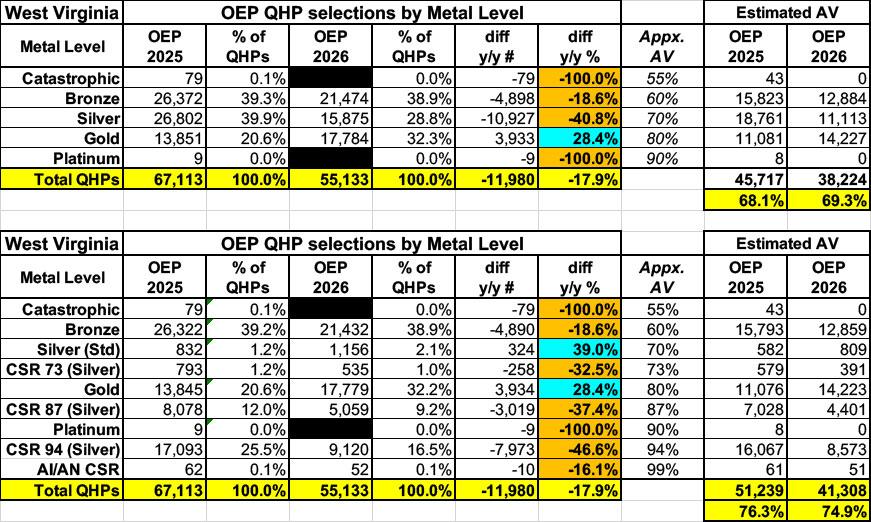

Here's total Open Enrollment plan selections for both 2025 & 2026 broken out by Actuarial Value (AV) category. The first table is based on official metal level tiers, but it's the second table which is critical, since a huge chunk of ACA enrollees are usually enrolled in CSR Silver plans (which include Cost Sharing Reduction assistance). CSR assistance dramatically boosts the AV of Silver plans up to Platinum levels in most cases.

As shown below, while many of the ~55,000 West Virginians who managed to survive the Open Enrollment Period did "buy down" to a worse plan, the actual net impact on average actuarial values actually didn't go down by that much: It dropped by just 1.4 points.

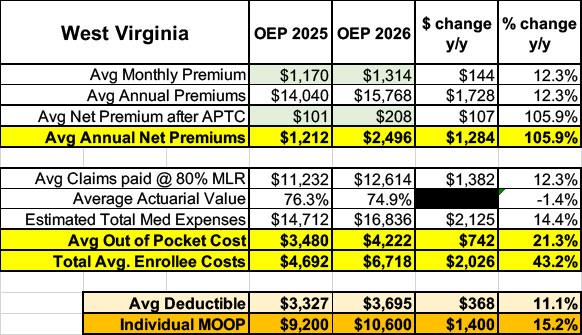

By combining these numbers with the average gross premiums per enrollee I'm able to calculate an estimate of the average total medical expenses each enrollee racks up each year assuming an 80% average Medical Loss Ratio (as I stated in the original post, this can vary widely by carrier and year, so should be considered a very broad average only), which looks like so:

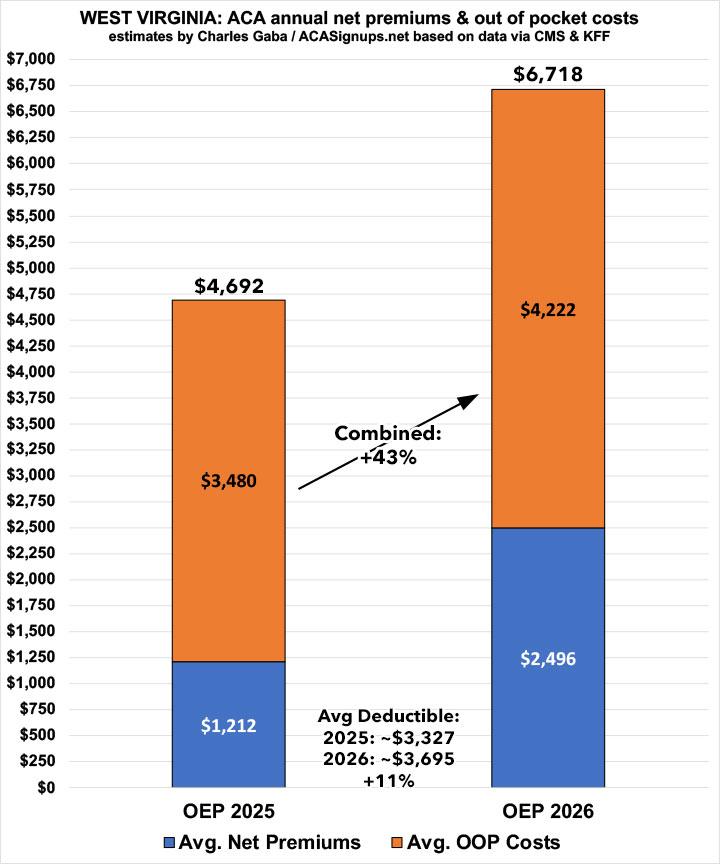

On average, net premiums more than doubled from $101/mo to $208/mo. In addition, by my estimates, average out of pocket spending shot up around 21% as well this year, resulting in a combined average 43% increase in total net healthcare spending...which amounts to around $2,000 more per year per enrollee.

Interestingly, based on KFF's net data, average deductibles also went up around 11%, to roughly $3,700 for single coverage. The maximum (theoretical) out of pocket cut-off for all ACA enrollees went up by over 15% this year as well, however, to $10,600 for single coverage.

Next up: WISCONSIN.

Advertisement